How to Map Your Financial Future with an SIP Return Calculator

Financial planning is an act of precision. The difference between a retirement that affords freedom and one that demands compromise often comes down not to how much was earned, but to how deliberately every rupee was directed.

Systematic Investment Plans (SIPs) have long been recognised as one of the most disciplined vehicles for long-term wealth creation. They bring structure to investing, reduce the need to time the market by spreading investments over time, and allow compounding to work over extended horizons. Yet the mere act of starting a SIP is only half the equation. The other half lies in developing a realistic estimate of where that investment could be headed.

This is precisely the function an SIP return calculator serves. It transforms a commitment into a projection, helping investors visualise potential outcomes across varying rates of return, contribution levels, and time horizons. While actual returns will depend on market performance, such tools play a valuable role in shaping informed financial decisions.

The Strategic Case for Using a SIP Return Calculator

Most financial tools are designed for the uninitiated. They simplify, they generalise, and in doing so, they often obscure nuances that matter to more experienced investors. A well-designed SIP return calculator can go a step further. It places key variables such as investment tenure, expected rate of return, and monthly contribution in your control, and translates them into assumption-based projections that support decision-making.

The principle of compounding, while familiar, reveals its full impact only when viewed across different scenarios. An SIP return calculator enables this kind of structured analysis, allowing investors to evaluate how varying assumptions may influence outcomes before committing capital. Actual returns, however, remain subject to market conditions.

What an SIP Return Calculator Actually Computes

At its core, an SIP return calculator is based on the future value of a series of periodic investments. It uses a standard financial formula to estimate how regular contributions may grow over time under a given rate of return.

T = P × ({[1 + r]^n – 1} / i) × (1 + r)

Where:

- T = Maturity amount (the total value of your investment at the end)

- P = SIP amount (the fixed amount you invest)

- n = Total number of SIP payments

- r = Rate of interest per period

Each instalment compounds for a different period. Earlier investments remain in the market longer and therefore contribute more significantly to the final corpus. This staggered compounding effect is what makes long-term SIP investing materially different from linear accumulation.

Image Source: Jio BlackRock

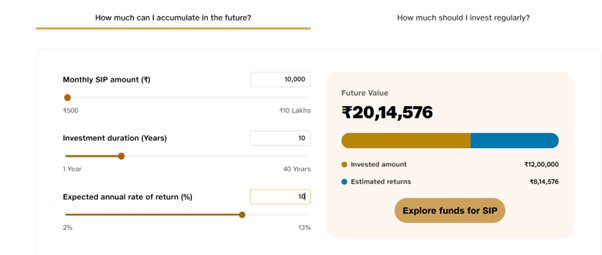

Scenario Mapping: Where the Real Value Lies

The true power of an SIP return calculator lies not in computing a single projection, but in comparing multiple scenarios side by side. Here is an illustrative analysis of how different inputs produce starkly different outcomes:

| Monthly SIP (₹) | Expected Return (p.a.) | Tenure | Total Invested (₹) | Estimated Corpus (₹) |

| 10,000 | 10% | 10 Years | 12,00,000 | ~20,14,576 |

| 10,000 | 12% | 10 Years | 12,00,000 | ~22,40,359 |

| 10,000 | 12% | 15 Years | 18,00,000 | ~47,59,314 |

| 20,000 | 12% | 15 Years | 36,00,000 | ~95,18,628 |

| 20,000 | 13% | 20 Years | 48,00,000 | ~2,07,69,703 |

Note: These are indicative figures based on assumed constant rates of return. Actual returns are subject to market conditions.

What this table illustrates is not just the value of higher returns, but the disproportionate impact of tenure. Extending the investment horizon, even at a constant rate, leads to non-linear growth in the final corpus. This is the effect of compounding over time, where earlier contributions continue to build on themselves, creating outcomes that are significantly higher than simple accumulation would suggest.

Integrating the MF SIP Calculator into Your Portfolio Review Process

Many investors review their portfolios periodically, often on a quarterly basis. Integrating a mutual fund SIP return calculator into that process transforms a retrospective exercise into a more forward-looking one.

Here is a practical framework:

Step 1: Anchor to Your Goal Corpus

Use the SIP calculator in reverse by entering your target corpus and working backwards to assess whether your current SIP contributions are aligned with that goal.

Step 2: Adjust for Inflation

If your goal is ₹2 crore in today’s value, the required amount over 15 years, assuming 6% annual inflation, would be approximately ₹4.7–4.8 crore. Some SIP calculators allow for inflation-adjusted projections, while in other cases this needs to be estimated separately.

Step 3: Model a Step-up SIP

Rather than maintaining a flat contribution, many investors increase their SIP annually in line with income growth. If supported, a step-up SIP scenario, where contributions increase by around 10% each year, can significantly change the projected corpus compared to a fixed SIP.

Step 4: Scenario-test Return Assumptions

Use a range of return assumptions, such as conservative (9%), moderate (12%), and optimistic (13%). This helps you understand how sensitive outcomes are to return variability and what level of return would be required to meet your target under different scenarios.

Common Errors Even Experienced Investors Make

Even the most methodical investors occasionally misuse projection tools. A few patterns worth guarding against:

- Anchoring to Elevated Historical Returns

Indian equity markets have delivered strong returns in certain periods. However, using assumptions in the mid- to high-teens as a base case can inflate projections and lead to underestimating the level of investment required to meet long-term goals.

- Overlooking The Impact of Costs

Mutual fund returns are typically reported net of expense ratios, but unrealistic return assumptions can still mask the long-term impact of costs. Additionally, exit loads, where applicable, may affect the final redemption value. Even small differences in effective returns can materially influence outcomes over longer horizons.

- Treating Projections as Guarantees

An SIP return calculator is a planning instrument, not a promise. Its value lies in enabling disciplined decision-making under different scenarios, rather than delivering precise predictions.

The Compounding Edge: Why Tenure Matters More Than Timing

There is a persistent instinct among investors to wait for the “right” market conditions before starting an SIP. Historical analyses across multiple market cycles often suggest otherwise.

For instance, investors who continued SIPs through periods such as the 2008 global financial crisis often benefited from lower purchase costs during market declines and participation in subsequent recoveries. The rupee cost averaging approach helps average out purchase prices over time, while compounding works more effectively across longer investment horizons.

What becomes evident in most SIP projections is that tenure plays a critical role in shaping outcomes. While returns matter, extending the investment horizon often has a disproportionately large impact on the final corpus.

The Discipline of Precision in Long-term Investing

An SIP return calculator does not tell you what the market will do. It helps you understand what your choices could lead to under a defined set of assumptions over a given horizon. That is a fundamentally different and more useful form of insight.

For investors who have already built the habit of consistent SIP investing, the next level lies in using these tools more deliberately. With the growing accessibility of online investment platforms like Jio BlackRock, investors today can combine disciplined planning with more informed execution. Start with clarity of purpose, validate it through structured scenario modelling, and allow compounding to play out over time.

Your financial future is not a destination reached by chance. It is shaped through deliberate decisions, refined over time, one projection at a time.

Pranab Bhandari is an Editor of the Financial Blog “Financebuzz”. Apart from writing informative financial articles for his blog, he is a regular contributor to many national and international publications namely Tweak Your Biz, Growth Rocks ETC.