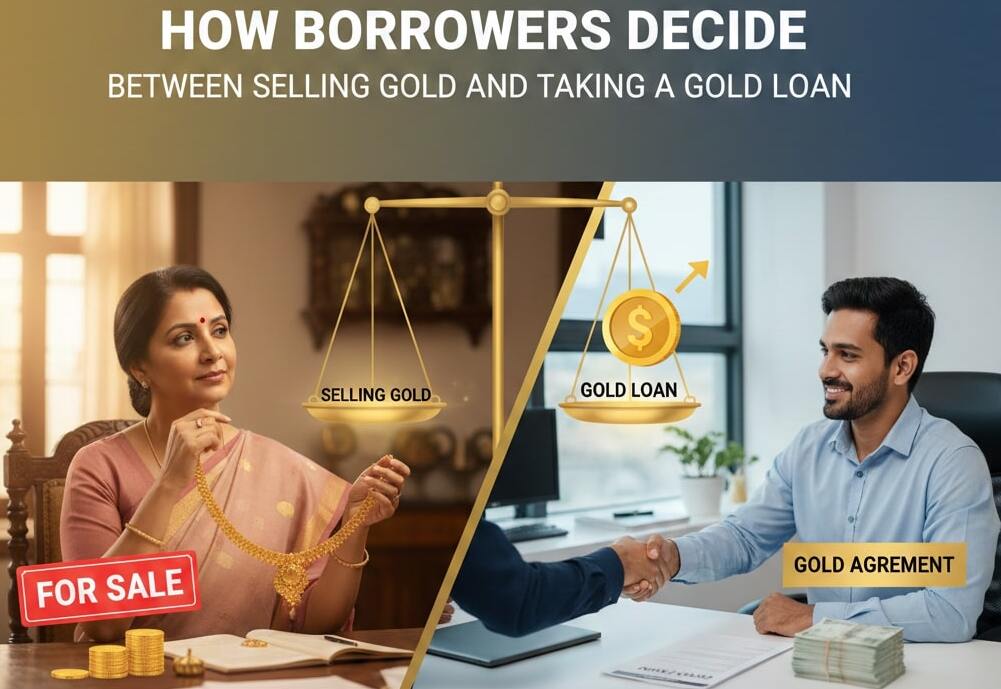

How Borrowers Decide Between Selling Gold and Taking A Gold Loan

For many Indian families, gold is the first asset they look at when a money requirement comes up. In that moment, one key question arises: should you sell the gold or use it to access a gold loan? Each choice has different implications for your liquidity, long-term wealth, and peace of mind.

This article explains how borrowers think through that decision, how RBI directions shape lending against gold, and how to weigh both options before you act.

Why is gold often The First Option For Short-Term Needs?

Gold plays more than one role in Indian families. It is:

- A form of savings that can be converted into money

- An emotional asset, often linked with family events

- A backup for medical bills, school fees, business cash gaps, and other urgent needs

Because of this, borrowers generally see two paths:

- Convert the gold into cash by selling it

- Use it as collateral and access funds through a gold loan

Recent RBI directions on lending against gold and silver aim to standardise how lenders value, store, and release pledged gold, which gives borrowers more clarity when they choose to borrow instead of sell.

What it Really Means to Take a Gold Loan

A gold loan allows you to pledge gold jewellery or ornaments and receive funds without permanently giving up ownership. The lender holds the gold as security and returns it once you close the loan.

When borrowers lean towards a gold loan, they usually think about:

- Control Over The Asset: You retain ownership of your gold as long as you repay the loan as agreed. For families that treat gold as a long-term store of wealth or a legacy asset, this is a key reason to avoid selling.

- Tenure And Repayment Style: Depending on the lender’s product design and RBI rules, you may get options such as periodic EMIs, interest-only payments with principal at the end, or a single bullet settlement. These structures can suit different cash flow patterns, from salaried income to seasonal business earnings.

- Gold Loan Rate Today: Borrowers usually check the gold loan rate today and compare it with the cost of other credit options. The focus is not only on the headline rate but also on processing fees, charges for delay, and the overall cost if the loan is kept for the whole tenure.

- Regulatory LTV Ratio For Gold Loan: RBI directions set caps on the LTV ratio for gold loans, which is the proportion of the gold’s assessed value that can be lent out. This protects borrowers and ensures lenders do not over-lend against the pledged gold. The actual amount you receive will depend on valuation, purity, and the lender’s internal policies within these regulatory limits.

When deciding, many borrowers use a gold loan calculator to estimate how much they may be eligible for and what their instalments could look like under different tenures. That gives a clearer picture of affordability before they pledge their jewellery.

What do You Mean by Selling Your Gold

Selling gold is simple: you hand over the ornaments or coins to a buyer and receive cash in return. There is no future repayment obligation, and no interest cost. However, borrowers often weigh several points before taking this irreversible step:

- Loss of an Asset: Once sold, the same gold may not be easy to buy back later, especially if prices move unfavourably or income does not rise as expected.

- Emotional and Cultural Value: Many pieces are linked with weddings, festivals, or family milestones. Even if selling solves an immediate problem, it may feel like a permanent loss.

- Future Financial Flexibility: Gold that remains in the family can support multiple emergencies over the years through Gold Loans. Once sold, that fallback option disappears.

- Tax and Documentation Considerations: Depending on how long the gold was held and how you acquired it, selling may have tax implications, and buyers may insist on specific documentation. Borrowers often discuss this with their tax or financial advisor before deciding.

Because of these trade-offs, selling is usually seen as a more final choice, while a gold loan is a way of monetising the asset without giving it up permanently.

Key Questions Borrowers Ask Before Choosing

When borrowers stand at the crossroads between selling and borrowing, they tend to ask themselves a few simple but powerful questions:

How Urgent And How Long is The Need?

Short-term cash flow gaps or a one-time obligation may align better with a gold loan, especially when you expect money inflows soon. Long-term or structural cash shortages may not be suitable for any form of secured borrowing.

Can I Comfortably Service a Gold Loan?

Here, borrowers look at:

- Current income and other EMIs

- Whether they can handle interest payments or EMIs on time

- What happens if income is delayed or irregular

What Does The LTV Ratio For a Gold Loan Mean For me?

If regulatory and lender limits mean the eligible loan amount is below the requirement, borrowers either reduce the requirement, pledge more gold, or explore another product altogether.

How Do I View Gold in My Overall Wealth Plan?

Those who see gold primarily as a hedge or family asset may prefer a gold loan so that the jewellery eventually comes back home. Others who treat it only as an investment may be more comfortable selling if the price is favourable.

How Does The Gold Loan Rate Today Compare With Alternatives?

Borrowers often compare the total cost of a gold loan with unsecured options and the opportunity cost of selling gold that might appreciate further. This helps them avoid taking on a loan that is more expensive than necessary for their situation.

Read More: Things to Keep in Mind While Applying for a Gold Loan Against Jewellery

Conclusion

Selling gold or choosing a gold loan is ultimately about balancing immediate relief with long-term security. Before you decide, be clear about how much you need, how soon you can repay, and how important it is to keep your jewellery within the family.

Use tools such as a gold loan calculator, check the gold loan rate today, and understand the LTV ratio for gold loans under the current RBI directions.

If the numbers still do not feel comfortable, review other borrowing options after checking your CIBIL profile. A calm, informed approach can help you meet today’s requirements without weakening tomorrow’s financial stability.

Pranab Bhandari is an Editor of the Financial Blog “Financebuzz”. Apart from writing informative financial articles for his blog, he is a regular contributor to many national and international publications namely Tweak Your Biz, Growth Rocks ETC.