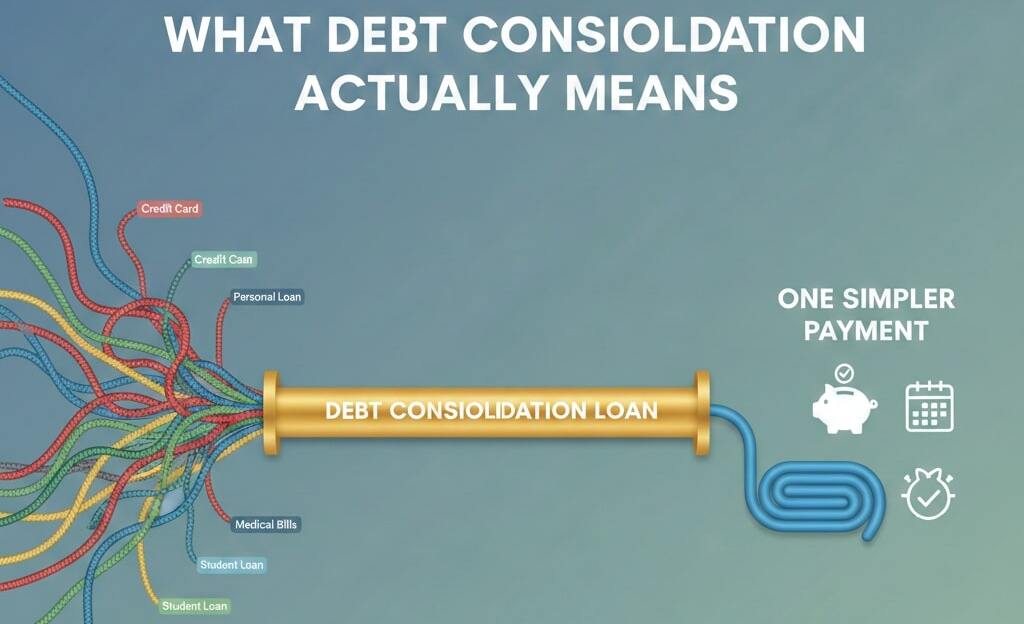

What Debt Consolidation Actually Means

Debt consolidation is one of those financial terms that sounds simple on the surface but often feels confusing when you try to break it down. Many people first explore it when juggling several bills at once or considering whether options like San Diego auto title loans could help them catch up. But consolidation is not about quick fixes or borrowing for the sake of borrowing. At its core, debt consolidation is a strategy designed to bring clarity, structure and relief to an otherwise overwhelming financial situation.

What Debt Consolidation Really Does for You

When you consolidate debt, you take several existing balances and roll them into one new loan or line of credit. Instead of paying multiple lenders at different interest rates and on different schedules, you make a single payment each month. The purpose is not only to simplify your financial life but also to save money over time. If your new loan has a lower interest rate than the debts you are paying off, more of your monthly payment goes toward reducing the principal rather than getting swallowed up by interest.

Why People Turn to Consolidation Instead of Managing Multiple Debts

For many, the biggest challenge is not the debt itself but the chaos surrounding it. Different due dates, minimum payments and fluctuating interest rates create a constant sense of pressure. Debt consolidation removes that confusion. It organizes your debts into one clear payment plan that is easier to keep track of. Chronically missing payments or struggling to cover multiple minimums can damage your credit. A single consolidated payment can help restore a sense of control and stability.

Understanding How Consolidation Loans Work

A consolidation loan is typically a personal loan, though other products like home equity loans or balance transfer credit cards can serve a similar purpose. When approved, the lender pays off your existing debts directly or provides the money for you to do it yourself. You are then responsible for paying back the consolidation loan over a set term. The terms vary by lender, but fixed interest rates and predictable monthly payments are common features. This structure allows you to plan your budget more effectively and avoid unexpected increases.

The Role of Credit in Debt Consolidation

Your credit score influences whether you qualify for a good interest rate on your consolidation loan. Borrowers with higher scores often access lower rates, which means greater savings over the life of the loan. Even if your credit is not perfect, consolidation may still be possible, though the benefits might be smaller. Understanding how credit impacts your consolidation options can help you make an informed decision. The Consumer Financial Protection Bureau’s guidance on personal loans offers helpful explanations of how credit influences lending decisions.

Why Consolidation Is Not the Same as Debt Settlement

It is easy to confuse debt consolidation with debt settlement, but the two are very different. Consolidation involves paying the full amount you owe through one streamlined loan. Debt settlement attempts to negotiate with creditors to reduce your balances. While settlement can lower the total you pay, it usually harms your credit and may involve fees. Consolidation, on the other hand, keeps your accounts in good standing as long as you make payments on time. It is a structured, predictable approach rather than a negotiation tactic.

How Consolidation Affects Your Monthly Budget

One of the immediate benefits of consolidation is a more manageable monthly payment. Because the interest rate may be lower and the repayment term potentially longer, you often end up with smaller monthly payments than the combined minimums from your previous debts. This breathing room can help you improve your overall financial health. With fewer bills to juggle, you can focus on saving, planning for the future or slowly building up an emergency fund. Predictability is one of the biggest advantages consolidation offers.

The Hidden Benefits People Don’t Always Consider

Beyond convenience and savings, consolidation can improve your relationship with money. When everything is streamlined into one payment, it becomes easier to track progress and stay motivated. You can watch your balance decline month after month instead of feeling overwhelmed by scattered statements. This psychological shift can help reduce stress and improve your mindset around debt. It encourages consistency, and consistency is one of the most important elements of financial stability.

When Debt Consolidation Might Not Be the Best Option

Consolidation is not ideal for everyone. If your current debts have very low interest rates or if you struggle with overspending, consolidation may only provide temporary relief. It is also not a magic fix. If poor spending habits or irregular income are the root causes of your debt, consolidation alone will not solve the problem. You need a solid budget, a commitment to making payments and an awareness of how you got into debt in the first place. The Federal Trade Commission’s advice on managing debt can help you evaluate whether consolidation is the right path.

Building a Long Term Strategy With Consolidation

Debt consolidation works best as part of an overall financial strategy that includes budgeting, saving and avoiding unnecessary credit use. Once your debts are combined into one loan, the goal is to make consistent on time payments until the loan is paid off. During this period, it is crucial to avoid taking on new debt unless absolutely necessary. This focused approach helps you eliminate debt steadily rather than bouncing between multiple balances.

A Clearer Path Toward Financial Stability

Debt consolidation is ultimately about clarity and control. It transforms a scattered, stressful financial situation into a single structured plan. By replacing multiple payments with one organized loan, you gain the mental space and financial stability needed to move forward. Whether your goal is to save money, reduce stress or rebuild your financial foundation, consolidation can be a powerful step toward long term stability.

Pranab Bhandari is an Editor of the Financial Blog “Financebuzz”. Apart from writing informative financial articles for his blog, he is a regular contributor to many national and international publications namely Tweak Your Biz, Growth Rocks ETC.