How Much Should You Spend on a Vehicle

“What the hell did you just do?”

My mind is racing and screaming at me.

My heart is beating faster and faster, my breath becoming shallower and more rapid. My knuckles are turning white from gripping the steering wheel.

Suddenly, the air in my truck becomes stale and hot. Sweat starts forming and rolling down my face.

The music is blasting, but I can’t hear it.

I’ve just driven my newly purchased Toyota Tacoma off the dealership lot. Fifty-five thousand dollars and a horrible loan term later, my body is starting to feel ill.

My stress and anxiety are rearing their ugly head. The massive hole I just dug for myself is starting to set in, and I’m staring up a climb that feels taller than Everest.

What was supposed to be an exciting time for a new car owner became a bit of a nightmare for me. Not because I had bought something I wanted, but because I knew the true cost of this car and how terrible a financial decision this was.

Buying this truck didn’t financially cripple me. I could afford the monthly payment many times over. I didn’t have to resort to eating cups of noodles every day to get by, and my day-to-day life didn’t take a step backward.

What did step backwards were my financial goals and investment strategy.

As I was driving home, a simple question came to mind.

How much should you spend on a vehicle to prevent this feeling?

My mind kept going around and around that question for the rest of the drive home.

It was such a persistent question for me that as soon as I got home, I started researching, ” How much should you actually spend on a vehicle?

Here is what I found.

The Simple Rules for How Much You Should Spend on a Vehicle

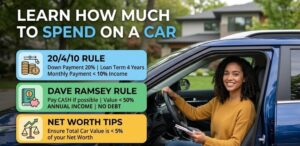

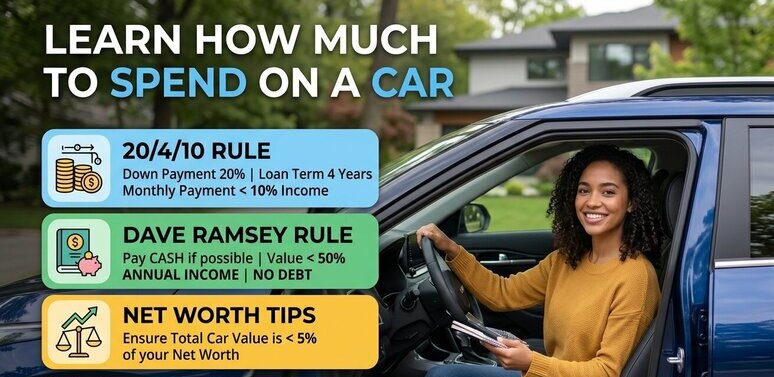

Rule #1: The 20/4/10 Rule

Following this rule means that you will put 20% down on the total purchase price (including taxes and fees), the loan term will be less than 4 years, and the payment will be less than 10% of your total take-home pay.

This rule is great if you don’t have enough cash to pay for the full price of the car. But it keeps you in a position of power with your finances. By that, I mean that you are still financially free to do what you want with your money on a monthly basis, even with the car payment.

You will not be eating rice and beans for months on end. You will still be able to save and invest for your future.

The cons of this rule are that you take out debt on a depreciating asset.

Rule #2: The Dave Ramsey Rule

Dave’s clear rule is that the value of all your cars should not exceed half your annual salary. Meaning that if you make $100k and only have 1 car, then the max you can spend on that car is $50k.

However, if you already have 1 car that costs $30k, then the max you can spend on that second car would be $20k.

Additionally, Dave is known for saying no to debt, so while earning a $100k salary means you can buy a 50k car, he doesn’t want you to take a loan out to buy that car. He prefers that everyone pay in cash when buying a car.

Pros of this method are that it keeps you from overspending your money on depreciating assets and keeps you out of debt.

Cons of this method are that you will need to have a decent amount of cash on hand to buy a car.

Rule #3: Buy Whatever Car You Want, Just Pay for it in Cash

This is the rule I personally prefer, and there are two reasons why.

First, some people genuinely love cars. They enjoy driving something exciting and take pride in what they drive. At the end of the day, life is short, and if driving a nice car makes someone happy, that’s their choice. If someone wants to drive a $100k car while making $80k a year, who am I to judge?

The second reason I like this rule is that paying in cash forces you to confront the true cost of the purchase.

When you finance a car, the dealership focuses your attention on the monthly payment. A $55,000 truck suddenly becomes “only $800 a month.” But when you pay in cash, there’s no hiding from the real number.

Using our $100k example, it likely took years of saving and discipline to accumulate that amount of money. Writing a check for that full amount suddenly becomes a much harder decision. Spending money that took years to earn feels very different than agreeing to a monthly payment.

The downside of this approach is that you may still spend more on a car than you reasonably should, and it requires having a large amount of cash available.

Rule #4: The 10% of Net Worth Rule

Another rule that I’ve heard is that the value of your car should not exceed 10% of your total net worth.

To illustrate:

- If your net worth is $100,000, then the maximum your car can be is $10,000.

- If your net worth is 500,000, then the maximum your car can be is $50,000.

- If your net worth is 1,000,000, then the maximum your car can be is $100,000.

The idea behind this is that someone who has a smaller net worth should focus on buying assets that appreciate instead of assets that depreciate.

The pros of this method are that it’s fairly straightforward and scales well for anyone’s financial situation. For example, someone just starting their career shouldn’t be driving the same car as someone who has been working for decades.

The downside of this rule is that someone who is just starting out in their career would likely have to buy a very inexpensive car. Additionally, this rule wouldn’t work for someone who has a negative net worth.

Different Ways to Think About Buying the Car

Most of us, when determining how much we should spend on a vehicle, only think about, “Can I afford the monthly payments?”.

But we really should be asking ourselves a list of completely different questions.

- What is the total cost of the car?

- Am I sacrificing another goal to buy this car?

- Why shouldn’t I buy this?

- Are my emotions talking, or is this coming from a place of logic?

- Did I add any friction into this decision?

By asking these types of questions, we move out of the emotional phase of the purchase and can make more logical decisions.

Would I Still Buy the Truck?

Absolutely not.

While the truck has been great to me, with no major issues, and it provides me the utility that I need.

But the cost was astronomical, and at the end of the day, I would rather have the $55k in my bank account instead of it tied up in an asset that is depreciating every day.

If I could choose again, I probably would have bought some beater truck for a few thousand dollars and drove that thing until the wheels fell off.

Because at the end of the day, a car’s purpose is solely to get you around town. Nothing more and nothing less.

Conclusion

At the end of the day, there really is no right or wrong answer for how much you should spend for a vehicle.

There are multiple rules or frameworks that you can follow, but those don’t understand you and your needs.

It’s good to understand them and test them out, but at the end of the day, you need to be asking yourself the right questions.

Will this car improve my life?

If the answer is no, then you probably shouldn’t buy it. But don’t stop with this one question, ask yourself more to come to a sound conclusion.

I know that if I had done this, I would have made a much better financial and life decision.

Sean writes about practical strategies to build wealth and simplify money decisions at Simplifying Personal Finance or on X. He focuses on long-term wealth building, financial goal setting, paying down debt, and couples’ finances.

Pranab Bhandari is an Editor of the Financial Blog “Financebuzz”. Apart from writing informative financial articles for his blog, he is a regular contributor to many national and international publications namely Tweak Your Biz, Growth Rocks ETC.